-

The Infrastructure Kingmakers

As the software-only outsourcing model crumbles, a new class of corporate winners is emerging. These are the Infrastructure Kingmakers. In a world where business value is dictated by the efficiency of running large-scale AI agents, the ultimate operational moat belongs to whoever controls the data centers, the cooling systems, the energy grids, and the silicon.

This shift has created a massive macroeconomic phenomenon known as Compute Arbitrage.

The Economics of the Sovereign Moat

To understand why the old IT outsourcing hubs are scrambling to reinvent themselves, look at how the physical cost of intelligence has been structurally altered. Consider the massive divergence in global compute costs:

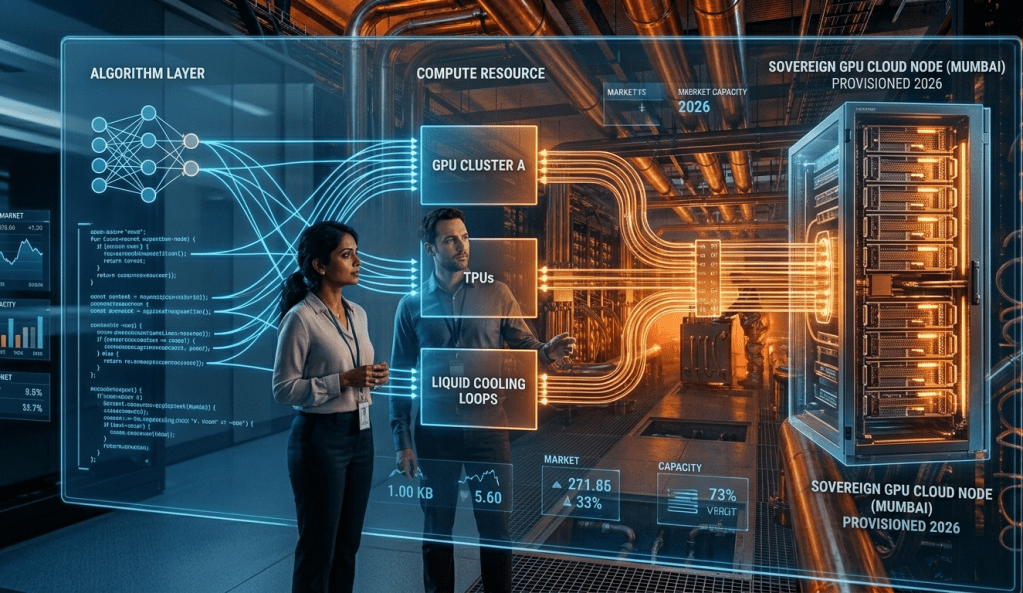

Metric Western Cloud Environments Subsidized Sovereign Infrastructure (e.g., IndiaAI Mission) Average High-End GPU Cost $2.00 – $4.00 / hour (On-Demand) $0.78 / hour (Subsidized Public Utility) Primary Power Source Grid-Dependent / Variable Pricing Solar-Backed / Green Energy Dedicated Operational Moat Software Subscription Fees Subsidized Capital Expenditure (CapEx) Because high-performance compute is increasingly treated as a public utility in emerging tech hubs, running private, specialized Small Language Models (SLMs) in a localized data center is now 30% to 45% cheaper than running them on a standard Western public cloud.

Moving Beyond the SaaS Premium

For years, Western enterprises paid a heavy premium for monolithic SaaS platforms. In 2026, those subscription fees are viewing a major correction. Forward-thinking Chief Financial Officers have realized they can leverage subsidized cross-border infrastructure to deploy internal, autonomous agents that manage complex corporate tasks entirely in-house.

The Concrete Shift: Why pay a massive recurring software seat fee when you can utilize an infrastructure partner to run custom, sovereign workflows that process everything from real-time global audits to hyper-localized supply chain variations for a fraction of the cost?

The winners of this paradigm shift are not the companies writing generic software wrapper apps. The winners are the architects who build the physical and structural plumbing—the optimization layers, the localized data enclaves, and the custom hardware arrays—that make enterprise intelligence incredibly cheap to scale.

-

The Death of the Code Factory

For three decades, the global technology services sector lived by a single, unshakeable metric: The Hourly Billable Rate. The math was clean. You took a software requirement from an enterprise in San Francisco or London, moved the execution to a lower-cost hub like Bengaluru or Manila, and pocketed the margin between Western salaries and local labor costs. This was Labor Arbitrage, and it built a multi-billion-dollar global industry.

Then came the infrastructure singularity of the mid-2020s.

By 2026, the underlying economics of writing software changed forever. The traditional “code factory”—where armies of junior developers spent weeks building APIs, writing boilerplate code, and running basic manual QA tests—has been entirely subsumed by autonomous engineering agents.

The Velocity Gap

The numbers are staggering and impossible for a human workforce to compete with:

- The Legacy Model: Top-tier legacy IT firms are seeing revenue growth stall out at single digits (2% to 6%).

- The AI Hyper-Scale: Foundational infrastructure platforms are experiencing meteoric, unprecedented revenue spikes as enterprises bypass traditional service layers.

The bottleneck is no longer human hands; it is raw, unadulterated cognitive processing capacity.

The New Structural Reality: If a software agent can generate, test, and deploy an enterprise-grade microservice in four minutes for pennies, billing an enterprise client for a “40-hour developer week” is no longer a sustainable business model. It is an economic fiction.

Why Pure Software Shops Are Stranded

Software-only outsourcing providers are discovering that their “proprietary platforms” were actually just expensive human labor wrapped in an adjustable software agreement. Without physical ownership of infrastructure, clean energy access, or proprietary data pipelines, pure-play software engineering shops are being squeezed out.

The enterprise buyer’s focus has permanently shifted. They are no longer asking, “How many developers can you assign to this project?” Instead, they are demanding, “What is your cost per reasoning step, and how optimized is your infrastructure to run our operational fleet of agents?”

The era of renting human fingers to type code is over. The era of managing raw compute efficiency has begun.

-

The PM & CIO Playbook – Navigating the “Hardware Bottleneck” in High-Stakes Contracts

If you are a Product Manager or CIO attempting to sign a high-stakes enterprise AI delivery contract right now, your biggest competitor isn’t another tech firm down the street. Your actual adversary is the global hardware bottleneck. If you promise a client custom model tuning, semantic search optimization, and agentic workflows without first securing your physical compute layer, you are signing a high-liability contract you physically cannot fulfill.

The Shift: Upstream Procurement as a Core Product Skill

In the cloud-native era, hardware was treated like a transparent utility. You spun up instances dynamically, scaled horizontally with a click, and rarely thought about the physical silicon beneath the code.

In 2026, that luxury is gone. Compute allocation has become a primary product KPI. Tech leaders can no longer build products in an architectural vacuum; they must design software that is deeply conscious of the underlying hardware constraints.

The Strategy: The 3-Step Hardware Guardrail for Product Leaders

To protect margins and ensure project delivery, Product Managers and tech executives must deploy a strict infrastructure playbook:

- Ditch Public Cloud Buffers: Relying purely on global hyperscaler on-demand capacity is a high-risk gamble. During peak global training cycles, public capacity gets heavily throttled or undergoes massive surge pricing. Top-tier outsourcing firms are mitigating this by securing fixed-rate contracts with local sovereign GPU clouds to guarantee predictable latency and unthrottled compute access.

- Enforce an Edge-First Architecture: Stop routing every trivial user interaction back to a multi-million dollar centralized cluster. Product teams must optimize their applications by utilizing smaller, highly specialized models designed to run locally on regional edge servers or on the client’s on-premise hardware. This preserves premium GPU clusters for high-value heavy lifting.

- Tie Performance SLAs Directly to Hardware Provisioning: Modern Service Level Agreements (SLAs) must be completely rewritten. If a enterprise client demands a 99.9% uptime on a highly complex, custom LLM pipeline, the contract must explicitly state the hardware allocation. Clients must either co-invest in dedicated physical nodes upfront or accept a variable performance tier based on real-time hardware availability.

The most brilliant AI model or agentic framework is entirely useless if it sits queued in perpetuity waiting for an available cluster slot. The future of global tech service belongs to the product leaders who know how to bridge the gap between elegant abstract code and raw physical silicon.

-

The GPU Factories – The Brutal Physics of the 5-Gigawatt Shift

You cannot run a 2026 enterprise AI strategy on a 2016 data center grid. Traditional offshore delivery facilities were engineered for standard x86 servers—built for steady, predictable workloads, low power draws, and standard forced-air cooling. The sudden pivot to multi-billion parameter model training and continuous fine-tuning has introduced a brutal reality check: the physical infrastructure of our tech cities is literally melting under the demand.

The Reality: From Server Racks to Power Plants

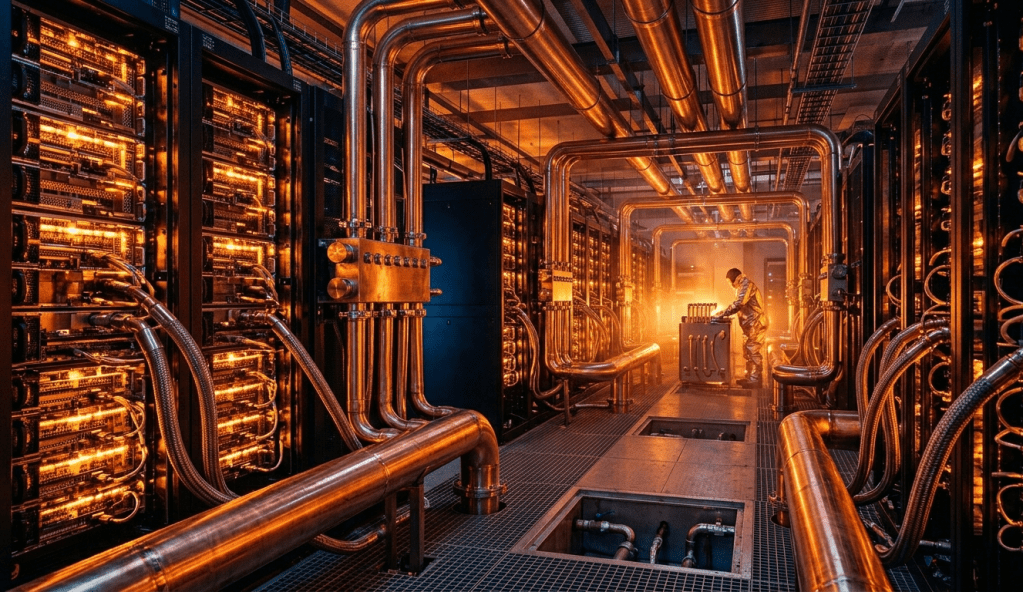

AI infrastructure requires an entirely different species of physical architecture. We are witnessing the rapid death of the traditional server closet and the rise of the “AI Factory”—gigawatt-scale compute campuses built exclusively for the intense, unbroken thermal load of the AI lifecycle.

Consider the staggering leap in hardware physics: a standard enterprise data center rack pulls roughly 5 to 10 kilowatts (kW) of power. An advanced AI-ready cluster pulling dense GPU arrays or custom application-specific integrated circuits (ASICs) requires anywhere from 40 to 100 kW per single rack.

This unprecedented energy and thermal density has triggered a massive, high-stakes hardware and civil engineering race across major technology hubs like Mumbai, Bengaluru, and Hyderabad:

- The Cooling Mutiny: Standard HVAC and raised-floor air cooling are utterly useless against modern chip clusters. Hubs are aggressively retrofitting legacy data centers for direct-to-chip liquid cooling loops and rear-door heat exchangers to prevent silicon degradation.

- The Power Land Grab: Data center capacity in India alone is on a blistering trajectory to explode from 1.6 GW to nearly 5 GW by 2030. Tech providers are bypassing city municipalities entirely to negotiate directly with state grids for dedicated high-voltage sub-stations and captive renewable energy plants.

- The Hardware Sovereignty Shield: Backed by aggressive government initiatives like the IndiaAI Mission and the semiconductor-focused ISM 2.0, local tech conglomerates are racing to anchor physical sovereign GPU clouds domestically. They are buying up silicon in massive blocks to insulate local enterprises from global geopolitical supply chain shocks.

+-------------------------------------------------------------------------+| THE INFRASTRUCTURE LEAP |+-------------------------------------------------------------------------+| LEGACY IT FACILITY || [Max 10 kW/Rack] ---> [Standard Air Cooling] ---> [Low-Margin T&M Code] |+-------------------------------------------------------------------------+| MODERN AI FACTORY || [40-100 kW/Rack] ---> [Liquid-to-Chip Loops] ---> [High-Value Inference]|+-------------------------------------------------------------------------+True enterprise AI transformation is no longer a software engineering challenge; it is a heavy civil infrastructure, thermal dynamics, and hardware logistics challenge.

-

The Compute Arbitrage – Why the “Software-Only” Outsourcing Model Just Died

For three decades, global technology hubs built empires on human capital. The formula was simple: hire the brightest engineering minds, seat them in a modern facility with standard business laptops, and bill western clients on a predictable time-and-material (T&M) basis.

But in 2026, that traditional software-only delivery model has collided with a hard physical ceiling. Clients are no longer asking engineering partners: “Do you have the developers to write this pipeline?” They are asking: “Do you have the dedicated physical clusters to run and test our models at scale?”

The Operational Friction: The Latency and Egress Trap

When global enterprises move from AI experimentation to production-grade deployment, they encounter an architectural nightmare. Moving petabytes of sensitive, proprietary corporate data back and forth across oceans to centralized Silicon Valley hyperscalers introduces crippling latency and catastrophic data-egress bills.

Furthermore, data sovereignty laws now dictate that enterprise data cannot freely cross borders for processing. The operational demand has shifted radically: global clients are forcing IT service giants in hubs like India, Poland, and the Philippines to host, fine-tune, and run inference locally within secure, regional boundaries.

The traditional cost advantage of offshore developer salaries is being completely overshadowed by the astronomical costs of unoptimized cloud infrastructure. If an IT delivery center relies entirely on public APIs, their margins are swallowed by the platform owners.

The Framework: The 2026 Outsourcing Maturity Matrix

To survive this shift, forward-thinking IT providers are aggressively restructuring their service catalog from a labor-first mindset to an infrastructure-first reality:

- The Legacy Tier (Rapidly Commoditizing): Delivering human bodies to handle basic software maintenance, manual QA, and legacy code migration. These margins are collapsing.

- The Transition Tier (Margin Squeezed): Building wrapper applications using external, expensive public APIs. These firms are highly vulnerable to hyperscaler pricing whims and client data-leakage anxieties.

- The Sovereign Tier (The New Elite): Owning or deeply partnering with the physical localized hardware layer to run private, secure enterprise inference on-site. They sell guaranteed compute time alongside engineering expertise.

Labor arbitrage is dead; it has been replaced by compute arbitrage. If your IT delivery partner doesn’t have direct, local access to high-density hardware infrastructure, they aren’t an AI transformation partner—they are just an unpaid QA team for big tech.

-

Architecting Contextual Moats.

Beyond the Algorithm: Building the Hyper-Localized Enterprise Engine

The first two parts of this series established a brutal double reality: hardware constraints are limiting the endless expansion of raw compute power, and global AI models are fundamentally blind to the implicit, non-digitized nuances of regional execution.

The corporate response to this double wall cannot be surrender, nor can it be to simply throw more capital at Western API providers. The solution requires a fundamental architectural pivot. Forward-thinking organizations must stop competing on the size of their foundational model and start competing on the depth of their proprietary context.

We are moving from the era of model-centric AI to context-centric AI. The ultimate enterprise asset is no longer the raw processing engine; it is the localized data moat built around it.

Building this contextual moat requires three structural transformations:

- The Extraction of Grassroots Knowledge: Organizations must design deliberate, structured pipelines to capture the implicit knowledge that lives entirely in the field. This means digitizing the unstructured operational wisdom of local distributors, regional sales leaders, and field engineers. If a critical market variable—like informal credit behavior or hyper-local infrastructure vulnerabilities—only exists inside a human head, it must be systematically captured, cleaned, and vectorized into an enterprise knowledge base.

- Architecting Small, Specialized Networks: Instead of routing every complex enterprise query to a monolithic, multi-billion-parameter global model that burns massive compute and hallucinates stability, architectures must shift toward ensembles of Small Language Models (SLMs). These lightweight models are highly optimized, exceptionally fast, cost-efficient, and trained explicitly on localized datasets. They don’t need to know the entire history of the world; they just need to master the exact operational mechanics of their target domain.

- Local Context Injection (RAG at the Edge): Foundational global models can still be used as general translation or reasoning layers, but they must be strictly governed by localized Retrieval-Augmented Generation (RAG) frameworks. Before an algorithm makes a predictive inventory decision or drafts a B2B sales communication, it must be forcefully injected with the real-time, ground-level constraints of that specific regional market.

By building proprietary data pipelines that prioritize deep local context over raw, brute-force processing muscle, enterprises can insulate themselves from global infrastructure shortages while achieving unprecedented operational precision.

The businesses that dominate the next decade will not be those with the biggest data centers, but those that successfully bridge the gap between global computation and hyper-local execution.

-

The Hallucination of Universality

The Cost of a Clean Dataset: Why Enterprise AI Stumbles at the Local Border

The boardrooms of the West share a dangerous consensus: that intelligence is a commodity scaling linearly with computational power. If an LLM can pass a bar exam, analyze a complex legal contract, or write functional Python script, it should easily optimize a distribution network or predict consumer behavior anywhere on the planet.

This assumption is not just wrong; it is financially hazardous.

What global AI strategies consistently miss is the difference between explicit data and implicit context. Global models are trained on the cleanly digitized, highly structured, and Western-centric open internet. They excel in environments where rules are written down, codified, and followed to the letter. But the moment you drop these multi-billion-parameter engines into a highly dynamic, hyper-fragmented ecosystem like the Indian market, the system fractures.

Consider the reality of a tier-2 or tier-3 distribution network in India. A global model looks at logistics data and assumes Western infrastructure parameters—predictable freight timelines, clear regulatory compliance structures, and formalized B2B communication.

It cannot calculate the operational gravity of localized variables:

- The informal credit networks built entirely on decades of multi-generational trust (“Kirana” dynamics) that dictate whether an order is accepted or rejected.

- The infrastructure micro-shocks—from sudden localized monsoon flooding to regional market closures—that never make it into a centralized database but live entirely inside the heads of regional on-ground distributors.

- The linguistic and cultural elasticity where a verbal “yes” or a specific phrasing in a regional market doesn’t mean a contractual commitment; it means a negotiation has officially begun.

When a global model encounters these unquantifiable realities, it does not stop and request more data. Instead, it does something far worse: it hallucinates universality. It forces the chaotic, hyper-localized operational reality into a clean, Westernized corporate template that it understands.

The result? AI-driven demand forecasting that misses inventory positions by critical margins, automated sales scripts that completely alienate long-term distributors, and strategic roadmaps built for an imaginary, perfectly organized market that does not exist on the ground.

Brute-force compute can buy processing speed, but it cannot buy cultural intelligence. Until enterprise AI architectures transition away from monolithic, top-down data structures and begin integrating localized, grassroots-level operational context, the “universal” model will remain an expensive corporate illusion.

-

The Sovereign Data Wall: The Night The Algorithms Hit the Ceiling

The Sovereign Data Wall: The Night The Algorithms Hit the Ceiling

For the last five years, the corporate mandate regarding AI has been singular: more compute, bigger datasets, and larger models. The underlying assumption was that universality (and compute power) would solve all contextual problems.

That assumption just hit a wall.

As detailed previously in our discussion on the “AI Tax,” physical compute infrastructure (GPUs, memory, power) is no longer a boundless commodity. Scarcity is the new default. But the true crunch is data. The internet has been scraped clean. The global datasets are digitized.

The easy part is over.

We are entering the era of Contextual Scarcity. The vast majority of valuable enterprise knowledge, proprietary cultural logic, and regional business practices—the subtle ‘know-how’ that actually powers an economy like India—remains analog, unstructured, or guarded behind corporate and sovereign firewalls.

This is the Sovereign Data Wall. Global models, facing a silicon squeeze and limited to Western-centric data pools, cannot simply brute-force their way through this wall. The AI model of the future cannot just predict generalities; it must operate within specific localized constraints. Organizations must pivot from managing hardware supply to cultivating proprietary contextual moats.

That is where the next decade’s competitive advantage lies.For the last five years, the corporate mandate regarding AI has been sing

-

Survival of the Optimized – Strategy in the Shortage Era

You can’t outspend a global structural shortage, so you have to out-think it. In 2026, the “AI PC” was supposed to be our savior—moving compute away from expensive clouds and onto our desks. But there’s a paradox: the hardware required to run AI locally is the very hardware that’s becoming prohibitively expensive.

The “AI PC” Paradox

To run a useful LLM locally, 16GB of RAM is no longer the “recommended” spec; it’s the bare minimum. 32GB is the new standard. As we saw in Part 1, the cost of these components is skyrocketing.

We are entering an era where the “Replacement Cycle” is dead. If you’re waiting for prices to “normalize” before refreshing your fleet, you might be waiting until 2028. By then, your competition will have already optimized around the shortage.

Three Pillars of the 2026 Strategy

- Inventory as a Financial Hedge: In a “Supercycle,” taking a bold inventory position isn’t just about supply—it’s a hedge against inflation. For those in the Stock & Sell motion, the “right” inventory is now more valuable than cash. If you have the hardware on the shelf, you own the market.

- The Shift to Edge & Hybrid AI: Instead of “brute-forcing” large models on every machine, winners are moving toward Edge AI. This means using smaller, hyper-optimized models that can run on existing hardware or specialized NPUs (Neural Processing Units), reducing the dependency on massive RAM/SSD clusters.

- Lifecycle Extension & Maintenance: If you can’t buy new, you must maintain. We are seeing a massive resurgence in component-level upgrades. Instead of replacing a $1,500 laptop, enterprises are spending $300 to max out the RAM and SSD—extending the ROI of their 2023/2024 investments.

The Conclusion

The winners of 2026 won’t be the companies with the most AI; they’ll be the ones who managed their hardware runway most effectively. The “Hardware Tax” is real, but it’s also a filter. It separates the companies that are just “chasing the hype” from the ones building a sustainable, hardware-aware AI future.

-

The Data Gravity Problem – Why SSDs are the New Gold

If RAM is the “brain” of the AI revolution, then SSDs (NAND Flash) are its nervous system. And right now, that nervous system is under cardiac arrest.

Data Gravity & the “KV Caching” Reality

AI models, especially Large Language Models (LLMs), don’t just process data once and forget it. They need a continuous “memory” of the context of a conversation. As these conversations get longer and the data gets heavier, a powerful pull—Data Gravity—occurs.

- The Problem: It is too expensive and energy-intensive to store all this heavy context in ultra-fast HBM/RAM.

- The Solution: Hyperscalers are offloading this “medium-term memory” to ultra-high-speed Enterprise SSDs.

- The Result: The rise of KV Caching (storing conversation context) has turned Enterprise SSDs into the most sought-after commodity on earth. Companies are building “All-Flash” data centers because “Just-in-Time” data retrieval is no longer optional for competitive AI.

The “Crumbs” of the Consumer Market

Just as we saw with RAM, this enterprise gold rush leaves the consumer and traditional IT markets with the leftovers. For businesses, this means the high-capacity QLC (Quad-Level Cell) SSDs you were planning to put into your workstations or standard servers are either:

- On allocation (meaning lead times of 3 to 6 months), or

- Selling at a premium of 70%+ higher than 2025 prices.

The narrative that “storage is cheap” is dead. In the age of AI, data has gravity, and that gravity is pulling the world’s highest-performing SSDs into a few select data centers, leaving the rest of the enterprise market paying the price.

The Strategic Takeaway for Leaders

- Validate Inventory: Don’t trust procurement forecasts. Confirm physical inventory before signing off on any major infrastructure project in 2026.

- Rethink Storage Architecure: Your business cannot compete if your on-premise infrastructure is bottlenecked by SATA SSDs. If you can’t afford the enterprise NAND, look at hyper-converged solutions that optimize existing storage.

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.